Major Axis regression(主成分回帰) Last modified: Aug 12, 2009

目的

Major Axis regression(主成分回帰)を行う

使用法

MA(x, y)

# print メソッド

print.MA(obj, digits=5, sig=0.95)

# plot メソッド

plot.MA(obj, posx="topleft", posy=NULL, xlab=obj$names.xy[1], ylab=obj$names.xy[2], ...)

引数

x,y 2 変数。

通常の回帰式と違い x,y は完全に対称的(式を変形するだけで y= にも x= にもなる)。

obj "MA" オブジェクト

digits 表示桁数

sig 信頼度(デフォルトで 95% 信頼限界)

posx, posy legend 関数のための位置引数("topleft", "bottomright" なども可)

xlab, ylab 軸の名前

... plot 関数に渡されるその他の引数

ソース

インストールは,以下の 1 行をコピーし,R コンソールにペーストする

source("http://aoki2.si.gunma-u.ac.jp/R/src/MA.R", encoding="euc-jp")

# Major Axis regression(主成分回帰)

MA <- function(x, y) # 2 つの変数

{

names.xy <- c(deparse(substitute(x)), deparse(substitute(y))) # 変数名を控えておく

OK <- complete.cases(x, y) # 欠損値を持つケースを除く

x <- x[OK]

y <- y[OK]

s2 <- cov(cbind(x, y)) # 分散・共分散行列

ev <- eigen(s2)$values # 固有値

b <- s2[1, 2]/(ev[1]-s2[2, 2]) # 傾き

a <- mean(y)-b*mean(x) # 切片

result <- list(names.xy=names.xy, x=x, y=y, ev=ev, intercept=a, slope=b)

class(result) <- "MA"

return(result)

}

# print メソッド

print.MA <- function( obj, # "MA" オブジェクト

digits=5, # 表示桁数

sig=0.95) # 信頼度

{

n <- length(obj$x) # ケース数

ev <- obj$ev

H <- qf(sig, 1, n-2)/(ev[1]/ev[2]+ev[2]/ev[1]-2)/(n-2)

CL <- tan(atan(obj$slope)+c(-0.5, 0.5)*asin(2*sqrt(H))) # 傾きの信頼限界値

ans <- data.frame(c(obj$intercept, obj$slope),

c(NA, CL[1]), c(NA, CL[2]))

alpha <- 0.5-sig/2

dimnames(ans) <- list(c("Intercept:", "Slope:"),

c("Estimate", paste(c(alpha, 1-alpha), "%", sep="")))

print(ans, digits=digits)

}

# plot メソッド

plot.MA <- function( obj, # "MA" オブジェクト

posx="topleft", posy=NULL, # legend 関数のための位置引数

xlab=obj$names.xy[1], # x 軸の名前

ylab=obj$names.xy[2], # y 軸の名前

...) # その他の任意の plot 関数の引数

{

plot(obj$x, obj$y, xlab=xlab, ylab=ylab, ...)

abline(obj$intercept, obj$slope)

abline(lm(obj$y~obj$x), lty=2, col=2)

legend(posx, posy, legend=c("Major Axis", "linear regression"), lty=1:2, col=1:2)

}

使用例

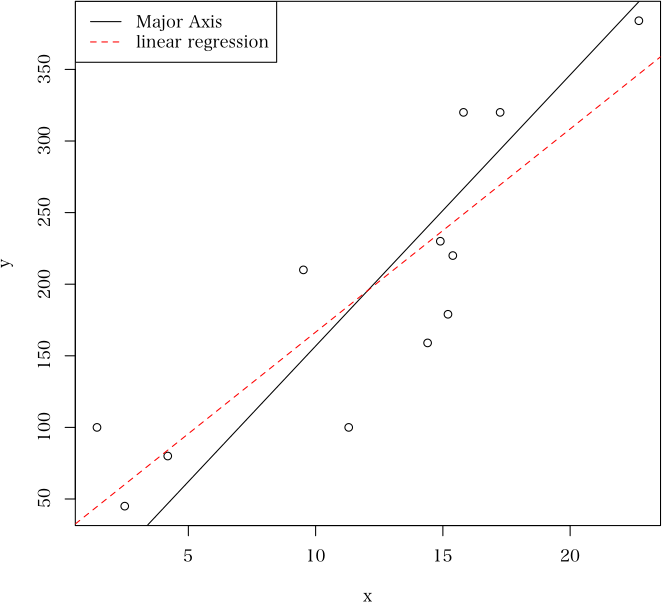

> x <- c(14.40, 15.20, 11.30, 2.50, 22.70, 14.90, 1.41, 15.81, 4.19, 15.39, 17.25, 9.52)

> y <- c(159, 179, 100, 45, 384, 230, 100, 320, 80, 220, 320, 210)

> MA(x, y) # 結果の出力には print.MA が使われる

Estimate 0.025% 0.975%

Intercept: -32.552 NA NA

Slope: 18.936 13.439 31.993

> x <- MA(x, y) # 結果を変数に付値する

> print(x, sig=0.99) # print メソッドで,信頼度を指定することができる

Estimate 0.005% 0.995%

Intercept: -32.552 NA NA

Slope: 18.936 11.967 45.138

> plot(x) # 散布図と MA による回帰直線を描く

直前のページへ戻る E-mail to Shigenobu AOKI

直前のページへ戻る E-mail to Shigenobu AOKI